Global fertilizer markets feel impact of conflict in the Middle East

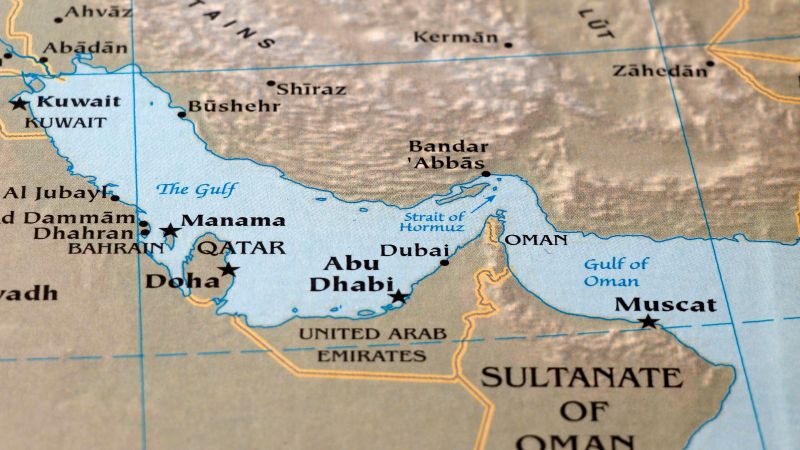

The Strait of Hormuz is a critical chokepoint for maritime traffic in the Middle East. The strait connects the Gulf of Oman and the portion of the Arabian Sea known as the Persian Gulf. On its north coast sits Iran and to the south, the United Arab Emirates and Oman.

The strait is a critical route for oil tankers from Saudi Arabia and other points. It’s estimated that over 20 percent of global oil and liquefied natural gas exports transit the Strait of Hormuz. The current Iranian conflict has implications for energy markets and the global economy.

In addition to oil supplies and lng, the Strait of Hormuz is also a critical bottleneck for the global fertilizer supply chain. Disruptions to maritime traffic through the Strait of Hormuz have an impact on global fertilizer supplies and prices as well as oil prices.

Eight months ago, Rabobank flagged the risks for global fertilizer markets of a potential Middle East conflict around the Strait of Hormuz. The conflict in June of 2025 now serves as reference point for the current Iranian conflict and its impact on this narrowest point in the global fertilizer trade.

The impact of the Iran conflict last year on global fertilizer markets was meaningful but ultimately contained. North African nitrogen fertilizer production was curtailed, which contributed to a sustained urea price premium throughout the year. The conflict also played a role in elevating global sulphur prices, alongside production issues in Kazakhstan and the Middle East, as well as export constraints from Russia. Still, because there was never a full closure of the Strait of Hormuz, the most severe scenarios were avoided in 2025.

This time, however, the situation is fundamentally different. The Strait of Hormuz is effectively closed—with vessel movements reduced to a trickle—and shippers are rerouting to avoid the Suez Canal. Insurance premiums have surged, LNG facilities have been damaged, downstream production (including urea) has been curtailed, refineries in Saudi Arabia are reducing runs, gas supply to Egypt is under force majeure, and European gas inventories are being reassessed. Taken together with current market pricing and fundamentals, these developments raise the risk that a prolonged conflict—especially one involving infrastructure damage—could push nitrogen fertilizer and phosphate markets toward a pricing paradigm distinct from that seen in the second half of 2025. This is not yet a forecast, but it is a very real risk.

As a result of this conflict, the fertilizer industry is concerned about potential declarations of force majeure, the most closely watched case being India’s recently awarded March‑delivery urea tender, where suppliers may now be unable to fulfil obligations. Force majeure claims could arise across the entire value chain.

A continuation of the current Middle East conflict could lead to an increase in fertilizer prices, Agricultural commodities have added a geopolitical risk premium though mostly indirectly—through higher energy prices and rising freight costs. Despite these pressures, global supplies across major ag‑commodities remain ample, limiting sustained upside. Fertilizers, however, operate under a fundamentally different dynamic. The Middle East is not just a transit route—it is central to nitrogen and ammonia production, and fertilizer markets are deeply tied to gas-linked production costs and regional energy prices. As a result, fertilizers are likely to absorb a far more persistent geopolitical risk premium.

Report Authors

Samuel Taylor

Senior Farm Inputs Analyst

Doriana Milankova

Senior Specialist, Farm Inputs & Sugar

Bruno Fonseca

Senior Economic Analyst

Frank Donker

Data Scientist

RaboResearch F&A

Disclaimer

This publication is issued by Coöperatieve Rabobank U.A., registered in Amsterdam, The Netherlands, and/or any one or more of its affiliates and related bodies corporate (jointly and individually: “Rabobank”). Coöperatieve Rabobank U.A. is authorised and regulated by De Nederlandsche Bank and the Netherlands Authority for the Financial Markets. Rabobank London Branch is authorised by the Prudential Regulation Authority (“PRA”) and subject to regulation by the Financial Conduct Authority and limited regulation by the PRA. Details about the extent of our regulation by the PRA are available from us on request. Registered in England and Wales No. BR002630. An overview of all locations from where Rabobank issues research publications and the (other) relevant local regulators can be found here: https://www.rabobank.com/knowledge/raboresearch-locations

The information and opinions contained in this document are indicative and for discussion purposes only. No rights may be derived from any transactions described and/or commercial ideas contained in this document. This document is for information purposes only and is not, and should not be construed as, an offer, invitation or recommendation. This document shall not form the basis of, or cannot be relied upon in connection with, any contract or commitment by Rabobank to enter into any agreement or transaction. The contents of this publication are general in nature and do not take into account your personal objectives, financial situation or needs. The information in this document is not intended, and should not be understood, as an advice (including, without limitation, an advice within the meaning of article 1:1 and article 4:23 of the Dutch Financial Supervision Act). You should consider the appropriateness of the information and statements having regard to your specific circumstances and obtain financial, legal and/or tax advice as appropriate. This document is based on public information. The information and opinions contained in this document have been compiled or arrived at from sources believed to be reliable, but no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness.

The information and statements herein are made in good faith and are only valid as at the date of publication of this document or marketing communication. Any opinions, forecasts or estimates herein constitute a judgement of Rabobank as at the date of this document, and there can be no assurance that future results or events will be consistent with any such opinions, forecasts or estimates. All opinions expressed in this document are subject to change without notice. To the extent permitted by law Rabobank does not accept any liability whatsoever for any loss or damage howsoever arising from any use of this document or its contents or otherwise arising in connection therewith.

This document may not be reproduced, distributed or published, in whole or in part, for any purpose, except with the prior written consent of Rabobank. The distribution of this document may be restricted by law in certain jurisdictions and recipients of this document should inform themselves about, and observe any such restrictions.

A summary of the methodologies used by Rabobank can be found on our website.

Coöperatieve Rabobank U.A., Croeselaan 18, 3521 CB Utrecht, The Netherlands. All rights reserved.